Success is doing the things that you love to do, and not doing the things that you don’t want to do. For Aunty to have the lifestyle she wants (and Uncle for his lifestyle), we need cash flow, profits, distributions. Build your wealth so you can enjoy your life.

Aunty did a post about selling on eBay a couple of years ago. Aunty also took (paid some bucks) an eBay course from an eBay guru who was a power seller. Truth to tell, Aunty did not use much of the information since a lot of it was for true rookies and some were for power sellers that are willing to devote all of their time loading, selling, packing, and shipping.

Aunty is more of a “hobby” eBayer, selling rarely and buying more often than she should.

However, since reading Marie Kondo’s book on the magical aspects of tidying up, piles of things that have value but no appeal or use are growing like mushrooms on Aunty’s floor. These are things that are someone else’s potential source of joy and in new or great condition, so eBay or Amazon are great venues that act like stores for Aunty.

Amazon

The easiest store is Amazon.com. One of the requirements is that you have the UPC or ISBN or manufacturing code from the packaging (best if you still have the box). If you have that, it is as easy a matter of entering the condition, number of items available, choosing a few options, setting your price, and SHAZAAM!, your listing is live. Amazon’s process will fill in the details, pictures, specifications, and your store is on the web. Listings remain on the site forever, until they sell.

Aunty uses Amazon mainly for books. Fulfillment by Amazon is a service that actually stores and ships out your items – one day Aunty actually shipped out an entire bookcase worth of books that were not being looked at – fees are higher but it was like a wall of freedom with blessed space!

Customer service at Amazon is fantastic. If you opt for a phone call from customer service, you WILL receive a phone call within minutes! The only downside as a seller on Amazon is that selling price points are very low, and if you don’t set your selling price low or lower, your inventory does not move. That being said, it is a great place to find bargains!

eBay

It used to be painfully difficult to sell on eBay. All of the descriptions were the responsibility of the seller, and photo editing, sizing, and uploading were time consuming and laborious.

Now, with the advent of eBay’s mobile app (eBay), it is super duper easy to begin a listing with the app, take all the photos with your smart phone, save the listing as a draft, and then use your computer to complete the listing. If you are a 100% mobile user, you could complete everything with your phone but the screen is much too small for Aunty’s aging eyes and scrolling is a pain. A computer screen allows Aunty to see the whole picture and more wonderful options reveal themselves, iAo (in Aunty’s opinion).

One of the new options is to enter the ISBN or whatever they call the numbers that manufacturers use to identify their items. Entering this will fill in a lot of the vitals of your items for sale, almost like Amazon!

The advantage of eBay being an auction site rather than a set price “store” like Amazon is that you could potentially get big bucks even if you don’t realize that your item is super desirable. Listings are usually on for just 7 days, but can easily be relisted if it does not sell, all for free. Fees are based on sales price, so if it sells, you pay. If it doesn’t sell, you don’t pay.

eBay also started a service that is almost like Amazon’s Fulfillment by Amazon program. eBay Valet will provide a shipping code and easy form to simply list the items that you want to sell (only certain items qualify), put them in a box and take it to a FedEx store, where it ships for free(!) to a “valet” who will do all the work and list your item(s) for sale on eBay. If it sells, you get a percentage and they take a percentage. Fees are rather high this way, but the convenience is wonderful. They are very picky about what they accept and will return the items that they reject. Aunty can attest to that – the valet returned most of the things that were sent and only listed a couple of the items. The good thing is that it didn’t cost Aunty a single cent to ship out or receive back the rejected items.

Shipping ease

Another great improvement is the ability to print shipping labels that have all the shipment info on it from your computer to your printer. The shipping costs (Aunty only uses USPS) are slightly lower than going to the post office and charged against your PayPal account. After the shipping label is printed, just trim, tape on the package, and pop it in the drive through mail box! They look super professional, with all the correct info, tracking number, and addresses printed in crisp black font. SUPER easy!

Danger

The greatest danger in using eBay and/or Amazon is the potential to shop and spend. Using their services to get cash for things that need to go out of the house is really terrific. Aunty loves seeing her Paypal account (acts as a bank to collect and pay eBay transactions) grow a little and grow a little more with each successful sale.

It is better not to look or search for items of interest on either site because you WILL find tantalizing treasures that will whet your appetite and draw your finger to the BUY button. Aunty’s weakness is Issey Miyake.

Buy, if you must, especially if not buying will become a regret. If you later decide that it no longer gives you joy, add it to the pile of “mushrooms” and sell it on eBay.

Michael Ford of the Palm Beach Letter (highly recommended) recently covered figuring out your magic number for retirement. Aunty likes to live comfortably – but it doesn’t just happen. Most people fall into 2 categories when it comes to figuring out their retirement needs: 1) procrastinators – those that put off or don’t really want to face what will be, and 2) pluckers – those that just pluck numbers out of thin air, making guesses. Aunty admits to being a plucker AND a procrastinator, but has since learned to do her homework.

Want to know your magic number? – that target figure that you will need to have in order to retire the way that you would like? This is the dollar figure of your investment/retirement account that will generate enough to replace your active (paycheck) income and pay for your expenses, continuously. Here are the rather simple steps:

Step 1 – Find your Lifestyle Burn Rate (LBR)

This is easy to do – calculate how much you are spending right now to live each year. [Aunty has Quickbooks “companies” for her business/investments as well as one for personal accounts. Quickbooks takes time to learn and input, but once done, it is SO convenient for accounting, taxes, and these kind of reports.]

It is easier if you group expenses into 3 basic categories: housing (mortgage, maintenance, taxes), basic living (food, clothing, health expenses), and entertainment (includes travel). Charity and education could also be 2 additional categories if you have expenses in those areas.

Add up all your expenses for each of these for the entire year (use last year’s figures) – this total will be your current Lifetime Burn Rate. Do not guess. You want to have real numbers that are true for you. You may also be surprised at what your number(s) look like.

If you are still young and without dependents, you have a low Lifestyle Burn Rate (stage 1). Your LBR dramatically rises after you have your first child, buy a house, pay for their education (stage 2). Then, after the kids leave the nest (stage 3), your LBR will be at least twice what it was when you were younger and carefree, but not as much as stage 2. If you are in stage 1 of your financial life, calculate your current LBR, and estimate for your future stages.

Step 2 – Adjust your LBR (Lifestyle Burn Rate) with extras or deductions

To reach your Retirement Lifestyle Burn Rate (RLBR), add in those extras that you want, i.e. weekly massages, more travel, gifts to grandchildren, golf club expenses. Then, subtract those expenses that you currently have but do not plan on having when you are retired. These expenses could be mortgage payments if you pay off the loan in entirety by the time you retire, less education expenses if you are still paying for your child’s college, less housing payments if you downsize.

This new number, your Retirement Lifestyle number may be larger, or smaller than your current Burn Rate.

Step 3 – Adjust your RLBR (Retirement Lifestyle Burn Rate) if you have any additional sources of income

These additional sources of income could include retirement pension payments, Social Security, part time work that you plan to do, etc. Whatever these add up to, slash the number in half (i.e. if Social Security, pension, and part time work is predicted to be $30,000 per year, divide by 2, leaving you $15,000).

After subtracting your anticipated additional sources of income from your RLBR, you will now have your Net Retirement Lifestyle Burn Rate (NRLBR). This number is a very important number. This is the dollar figure that you will need every year to live the lifestyle that you want when you retire.

Step 4 – What rate of return will you be getting on your savings/investments?

Hopefully you have savings or investments that generate income for you. If you do not, start today and build up your savings and investment portfolio. [This is the reason why Aunty took RichDad classes – even without doing this exercise of LBR, RLBR, NRLBR. Aunty knew we were in trouble, and that we needed to generate passive income for our retirement needs. One of the best ways, in Aunty’s opinion, is tax free with a Roth IRA. Even better is with a checkbook Roth IRA that controls real estate, short or long term capital gains, note lending, etc.]

Calculate what you currently make on your current available funds/portfolio. Then figure out the after tax total. This after tax net income divided into the portfolio total value is your current rate of return on your investments/savings. This number might be as low as .5% (YIKES!) if you have all your money in a bank savings account. Hopefully it is much higher, with dividends from stocks paying at least 3%, real estate rental income paying out 10%, income from other investment vehicles such as notes, bonds, etc.

Be very realistic with this. Do not make up a percentage based on what you wish you had.

Step 5 – Calculate your Magic Number

Take your NRLBR (net retirement lifestyle burn rate) that you got from Step 3 and divide it by your expected rate of return (from Step 4).

THIS is your Magic Number! This is the amount you need in your investment/savings/portfolio. How does it look?

If you have a lot of retirement income from your pension plan – i.e. a retired Hawaii State worker, you are in pretty good shape. However, it might still be a good idea to have additional income from investments, don’tcha think?

Aunty went to a HiMa (Hawaii Internet Marketing) meeting this week. Aunty joined a few months ago – not sure why since Aunty is a non-techie, non geekie, non-social media type – but the folks that run it are super nice and they always have pizza and water, and interesting subject matter.

The recent meeting was about finding our life’s purpose. What a big topic – but, what the hey, if anything, there would be pizza, right?

The guest speaker was Lani Kwon, a life coach, mother, speaker, and transformer. After a few minutes of intro, tidbits and pleasant stories, the nitty gritty happened when we started filling out some worksheets.

The first question was, “What would you do if anything were possible?” Sounds simple enough, but take a few minutes and ask that question of yourself. Anything. Nothing holding you back, the sky and beyond, no limits. You have a free pass to life’s candy store.

We were then walked through a series of questions about what holds us back, what keeps us stuck, what we need, visualization, solutions, action planning. The last step of the night was signing a contract with ourselves. A very simple contract. Commitment.

One’s life purpose(s) can seem very selfish because it is personally fulfilling. However, there is nothing wrong with figuring out what we want and then getting it, unless it is harmful to others.

Perhaps it is time for Aunty to finish up tidying, turn off Korean dramas, put away excuses, and dive in and commit to her life purposes.

Lani Kwon has tickled the tiger (actually, Aunty is a dragon). Awakening the dragon, hmmm. To quote German writer and statesman Johann Wolfgang von Goethe, “Whatever you can do or dream you can, begin it. Boldness has genius, power, and magic in it.”

Please sit down and take some time to figure out your life purpose. Please share, if you are willing.

Ever since Aunty turned 55 almost a decade ago, Tuesdays at Ross Dress for Less became her favorite shopping excursion because they gave 10% off to seniors.

Pal Jim turned Aunty on to Cardpool.com and Aunty could buy Ross (and other) gift cards at 20% savings. However, over time, Cardpool offered less and less of a discount, and recently Ross cards, if available, were at a 13% savings, which is still a good deal, especially when shopping on Tuesdays and also getting the senior 10% discount.

Then, just last week, hanabata days (from kid time) pal Cookie said, “Eh, you heard of Raise.com?” Pal Cookie is a shopping guru on steroids. She knows everything about everywhere and finds the best bargains and products all over the place.

“Better than Cardpool.com?” Aunty asked. “Go look”, she said, and Aunty did.

OMG – better than Cardpool.com because the discounts are higher and there are more retails stores in the offerings. Aunty just purchased her Ross gift card at 18% savings – woohoo! When it arrives in the mail, Aunty is going shopping at Ross’ on Tuesday with a 28% (18% + 10%) discount pass in hand!

It is also a site to search and search because discounts vary for each establishment depending on the dollar value as well as the day of the week. According to Cookie, Fridays are good bonus days to buy cards because they sometimes have an additional 5% discount thrown in the mix! They also run “specials” which can be easily found on the left of the menu.

On top of that (this is killing Aunty because it just keeps getting better and better!), Raise.com offers $5 credit to referred newbies after the first purchase – one credit to the newbie and one credit to the referrer!

When you sign up, you will get a user name that is made up of the first letter of your first name and the rest of it with your last name. (hint: if you want a custom user name, put a first letter in the first name line and the rest of the name in the last name line. Example, “aunty” was entered as “a” in the first name line and “unty” in the last name line. You can then change your name in your profile afterwards, but you will not be able to change your user name – ever. Another example, if you want “jalna” as your user name, enter “j” as your first name and “alna” as your last name. Change your first and last name after you complete sign up.)

After you get signed up, then you can refer people to sign up with emails, facebook, etc. When they come to the section of referral code, they enter your user name (like “aunty”, ahem) , and BAM! you get $5 and they get $5. Reminds Aunty of Paypal when it first started years ago. Rewards for referring people to join earned both parties $5. Then, Paypal got so huge and popular, it didn’t need referrals anymore.

Even if Raise.com didn’t give referral credits of $5, Aunty still thinks it is a great place to acquire discounts from favorite stores such as Whole Foods, Apple Store, Taco Bell, oh my! This is going to be delicious dangerous research into forced shopping due to purchased savings.

Much mahalo to Pal Cookie for her great tip and helping Aunty to spend money. To shop is human, to share discounts is divine.

*Update, update!!! Aunty was very pleased with her new Ross gift card and was going to shop with it. However, something told Aunty to check the card first. These cards come from somebody else – someone who is selling their card.

On the back of the gift card is a toll free number to Ross’ balance inquiry customer service line: 1-800-798-4055. Aunty followed the prompts, then put in the gift card number followed by the # key. Blip blurp oh oh, Aunty was informed that this card account was closed. Closed? Yikes?!!

So then, Aunty called the Raise Member Services number: 888-578-8422 and waited for an available customer representative. After a few minutes, Aunty got Bryce – a very nice young man who apologized and informed Aunty that sometimes cards are invalid for various reasons. Raise.com has a 100 day money back guarantee (so check or use your cards quickly, fellow shoppers!) and the refund process was begun. Phew!

Will Aunty use Raise.com again? You betcha! Aunty was impressed with Bryce’s niceness (Bryce, nice, get it? heh heh heh) and also the money back guarantee. Aunty’s shopping excursion to Ross’ will have to wait for another Tuesday in the near future. Perhaps that is a good way to save money, sort of.

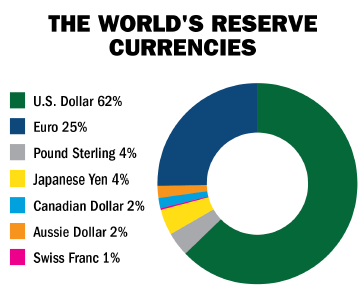

Recently, Aunty has been reading about the Chinese yuan (or renminbi) becoming a world reserve currency when the IMF (International Monetary Fund made up of international bankers) meets in October. If this happens, then international trades, purchases, exchanges, etc. can be done with Chinese money. Currently, the US dollar is the dominant trade currency, followed by Euros, English pounds, and Japanese yen. Adding the Chinese yuan to the mix may have extreme financial consequences.

What is a world reserve currency?

It is the acceptable form of money for international trade, and somewhat regulated to ensure that it is kosher. If Timbuktu wants to buy oil from Saudi Arabia, Timbuktu needs to buy US dollars (or another world reserve currency) to complete the the purchase. In the older days, gold was the standard of trade. In today’s fast and frenzied world, the standard of value for trade is any of the world reserve currencies, and more than likely, the US dollar.

China is scary

The US and China are rivals, yet they are very much dependent upon each other. China can materialize fake growth (building empty cities), manipulate financials, and act with impunity (no fear of consequences). It is a communist country with a controlled citizenship, sort of like the Queen of Hearts from Alice in Wonderland. China owns a lot of US dollars as well as a lot of our US debt. The US is the largest buyer of Chinese exports.

If the yuan becomes a world reserve currency, what can happen?

Some experts say that it can be a huge opportunity to building wealth. That sounds pretty good, and then the next question would be, “HOW?” since we already know the WHEN – October 2015. [Update: it didn’t happen at the IMF October meeting in Peru this year – so experts are now predicting NEXT year October 2016.]

BAIDU and BABA

Recently, Aunty was playing with these 2 Chinese company stocks which are traded on the US stock market. BAIDU is the Chinese equivalent of Google, and BABA the equivalent of eBay. Billions of people, badabee badaboom, Aunty played some options (a future post) on both stocks and then the dang Chinese government began to de-value the yuan.

What is going on with that scary country? Aunty likes their food but not their moves. After a financial whack on the hand (not too bad), it was time to visit some experts.

Stansberry’s Sjuggerud strategies

Aunty subscribes to tons of newsletters. Some are free, some are cheap, some are not so cheap but come with money back guarantees. Stansberry Research was either free or cheap and their daily emails are very informative. Dr. Steve Sjuggerud (pronounced sugar rude) is one of their advisors, and just the other day, his offer to subscribe to his monthly newsletters came with some timely bonus reports about how to benefit from the yuan becoming a world reserve currency. For $39, Aunty subscribed for a year, and got the bonus reports with the potentially wonderfully profitable advice. Here they are, in a nutshell:

Funds A few were a little beyond Aunty’s comfort zone such as certain Chinese bond funds or opening an account with Everbank. FXI (iShares China Large-Cap Fund) sounded pretty good since it is a fund that holds China’s 50 biggest and best companies that trade in Hong Kong, but Aunty is not sure about its fees.

House Another bonus report was about taking advantage if the US dollar becomes weaker by getting into investments that act like a hedge (protection). The hedge was to buy a house. The reasoning is that interest rates are so low and that homes are at bargain prices right now. Okay, it may be true about interest rates, but houses in Hawaii are NOT at bargain prices. Still, Aunty tends to think this is a good idea, even in Hawaii, and almost dreads to think of what will happen to our real estate once rich Chinese people decide to buy in Hawaii.

Stock Related to housing and in the real estate game of buy, fix and sell is the Blackstone Group, stock symbol BX. Currently it is $38 and it pays dividends. With its current pricing, the dividends return 7%! Hmmm. This is a looker! [Update Aug 2015: Almost all stocks took a beating after the Chinese government AGAIN devalued the yuan. BX dropped to $32 and is recovering. At current pricing of $34, it now provides dividend income of 8%, which is not shabby at all. Still, only invest what you are willing to lose if you cut your losses.]

Gold and silver This was not surprising – in times of uncertainty, precious metals are safe havens. However, rather than buying ETFs (exchange traded funds that “hold” gold and silver for you) or bullion or bars, the recommended investment are collectible coins, specifically older gold Saint-Gaudens or Morgan silver dollars, in MS64 or MS65 grades. (Aunty forgets how she found him, but Rich Gordon is the man at Eastern Numismatics. If you want to start off with a coin of interest or a roll of Silver Eagles, ask him for his help and expertise at (800) 835-0008 ext. 2300. He accommodates us Hawaii people by burning the New York midnight oil and calling his Hawaii clients late in the day or early evening.)

Sharing is caring

Aunty is not sure if sharing this info is against the subscription rules. If it is, then please, somebody let Aunty know and this post comes down. Aunty has a feeling that Dr. Sjuggerud’s True Wealth newsletters will be very worthwhile reading. Hopefully you will find his advice here to be worthy of thought, if not action.

Meanwhile, Aunty still likes BAIDU, and BABA. It is just too bad that they don’t seem to care about Aunty.

One of Aunty’s favorite quotes is: Life can only be understood backwards, but must be lived forwards. (Soren Kierkegaard)

To wit, there are moments in history that come upon us as surprises, but after they occur, we get a different perspective looking back and thus realize that the outcomes were predictable because of what happened prior to.

The crash of 2008

A good example of this was what led to the housing crash in 2008. Real estate earlier was booming because everyone and anyone could qualify for mortgages. Daughter #1 bought her first house in Las Vegas with very little down, and she didn’t even have a real job yet! Prices of homes crept up and up and it seemed as if anyone who wasn’t buying as soon as possible was a dummy.

This was the era of subprime lending. It was too much, too fast, and too easy.

When the party ended, banks, homeowners, and communities were smashed. It was devastating, and bankruptcies were at record highs. During the peak, it was difficult to see that this housing bubble would burst, but once it did, it seemed inevitable.

From the rubble

In Michael Moore’s 2009 movie, “Capitalism, a Love Story”, investors who swooped in and scooped up properties that had suddenly lost more than half its former value were called vultures. Vultures were evil and vile, predators of poor victims on hard times. Uncle and Aunty went to see the movie and felt perplexed after the show – we were investors, not vultures.

We bought short sales, and rented back to the former owners. We bought bank foreclosures, helping to keep communities stable. We were careful and did not over extend ourselves. We invested using Robert Kiyosaki’s Rich Dad principles.

Slowly, the market began to stabilize and improve. Looking back, an innovative and vibrant place like Las Vegas would survive, people always need a place to live in, and houses were of good quality selling for less than the cost to build. We unknowingly bought at the best time.

And now – Short window of opportunity

We just completed our home refinance – Hallelujah, happy dance, happy dance! It was grueling for Aunty because of our rather complex situation, but it was worth every paper scan and search now that it is complete. Our monthly expense for our mortgage is now much less than before. In Aunty’s opinion, the best deal in town are low mortgage interest rates – and they are not going to last much longer.

Can rates get lower? Very doubtful. Janet Yellen of the Federal Reserve Bank has been hinting about raising rates because our economy is improving.

Is our economy improving? Aunty thinks so. There are more new cars on the road now, more old furniture on the streets, meaning people are buying new things again.

Will rates go higher? Let’s see – hints by the person in control of rate hikes (Janet Yellen), people spending money again, housing prices climbing, job markets improving = good indicators that money will become more expensive via higher interest rates soon. [Aunty gets daily mortgage rate updates and interesting tidbits from paul.tamashiro@guaranteedrate.com. Email Paul if you also want to get daily updates. No pressure, just a very nice person.]

However, time is of the essence, and lenders are very strict.

Aunty and Noreen Ho (808) 398-8528

Not to despair, Noreen Ho to the rescue!

Aunty loves banks and bankers. Unfortunately, they don’t love Aunty. Remember the bank that says “yes?” Too many times, they checked out Aunty and say “no.” So rude.

It is because bankers must follow bank rules and are paid by salary. They can only offer you their own bank’s programs and cannot go shopping for you. Their number one bread and butter is their employer.

Mortgage brokers are free agents and are paid by commission. Their number one bread and butter is you, so if one lender says no, they will shop until they find one that wants you.

Noreen found us Provident Lending because they had the best rates, and a credit instead of points to pay! Aunty will tell you the truth, though. They are TOUGH and strict. However, once everything was in order, Noreen arranged the easy closing with Kevin of First American Title Company.

Noreen is THE best mortgage broker we have ever had the pleasure of using. We first met her because she was also a traveling notary public when we bought properties in Las Vegas and needed to sign docs. She is professional and also very nice. She really listens to what her client wants and will bend over backwards to get the job done. (She also looks MUCH better than this picture.)

Borrow to save, save to invest, invest to cash flow

Aunty should be retiring soon. Retired people will not qualify for mortgage loans because they do not have active income from paychecks. So…. refinance before you retire. If you are young and working, buy your parents’ home from them and then rent it out to them. Or, find an investment partner – they put in the down payment, you get the loan – profits and/or cash flow are split equitably.

You may think that it doesn’t make sense to have more, or extend more debt, but this is one of those look-back opportunities as interest rates begin to climb again. You will be glad you have a long term mortgage at historically low rates.

Loans are on sale but your banks are limiting supply. If you want to have the best mortgage broker working for you, please give Noreen Ho at Savvy Realty and Loans a call. (808) 398-8528. Tell her Aunty sent you and maybe we can all go to lunch together one of these days.

Aunty likes to talk to strangers, especially when waiting in lines or when nothing is going on.

At Kozo Sushi Kahala, Aunty was next to KITV4’s strikingly beautiful news anchor, Yunji deNies. Yunji was one of the MCs at the recent Cherry Blossom Festival Ball, so not only was she kinda famous, she was also kinda connected, if you understand local da kinds.

Anywho, Yunji was really nice and friendly, and she also shared a great tip with Aunty! It is the Bishop Estate’s free Malama app that gives discounts at many businesses that are located on Bishop Estate properties (i.e. LOTS of places such as most of the shopping centers and malls). The neat thing about it is how it can pull up the discounts based on where you are geographically on the islands. She whipped out her iPhone, and she got her sushi platter at Kozo for a special price!

It was so easy to download the Malama app. If you have a hard time doing so, visit the helpful people at any Apple Store. Update note: This app freezes if you have the latest operating system on iPhones. Aunty didn’t upgrade to the ios8 so her Malama app still works. Hopefully the good folks at Kamehameha Schools fix this glitch in the near future.

Key elements of the Mālama Card iPhone Application:

GPS location and merchant map

Users will have the ability to opt-in to sending GPS coordinates via their iPhone. Once a user opts-in, the application will use this GPS information to pull up a list of merchants and promotions nearest them.The application will display direction, north, south, east and west (N-S-E-W) and how far away the users are from each merchant in meters.We’ve also built in a merchant map screen that shows all Mālama Card merchants on a map along with the user’s current position. This enables the user to browse through all merchants in their area.

Virtual merchant and promotion list

The Mālama Card iPhone application is an alternative method for viewing merchants and promotions available through the Mālama Card program.Giving users access to merchant and promotion lists will make it easier for potential customers to see the value of the Mālama Card program.

Virtual Merchant profile screen

Each Mālama Card merchant has their very own profile screen in the Mälama Card iPhone application. The merchant profile screen displays contact information, address, web address and telephone number.Users can tap the merchant’s web address to view more information directly on their iPhone. Users can also tap the merchant’s phone number to launch the phone utility and send a call to the merchant.

Social media integration

Users can connect to their Facebook and Twitter accounts to send status updates on savings and discounts from the Mālama Card iPhone application. Users can also send an e-mail message to their friends directly from the merchant profile screen.

Virtual Malama Card

Once a user sees a discount they would like to take advantage of, they can tap the “Virtual Card” screen to launch an electronic version of the actual Mālama Card. Customers can show their iPhone to the merchant to redeem their discount or promotion.

All Mālama Card merchants are located on Kamehameha Schools’ commercial properties. These properties include Royal Hawaiian Center, Windward Mall, Pearlridge Center, Kahala Mall, Kapālama Shopping Center, as well as Waipahu, Waiakamilo, Kaka’ako, Keauhou, and Hawai’i Kai. Income from the school’s commercial leases fund KS’ campus and community outreach programs throughout the state.

Kamehameha Schools is a private, educational, charitable trust founded and endowed by the legacy of Princess Bernice Pauahi Bishop. Kamehameha Schools operates a statewide educational system enrolling more than 6,900 students of Hawaiian ancestry at K-12 campuses on O’ahu, Maui and Hawai’i and 31 preschool sites statewide. Approximately 37,500 additional Hawaiian learners are served each year through a range of other Kamehameha Schools’ outreach programs, community collaborations and financial aid opportunities in Hawai’i and across the continental United States.

Isn’t this a nifty app to have – save money at all kinds of places, all over Hawaii, for free? Yunji got her Kozo Sushi Kahala discount on sushi platters right off the bat. Next time, Aunty will too, as well as 10% off at one of Aunty’s favorite lunch places next door, Ba-Le (note update: Ba-Le doesn’t honor the discount. Oh well, it is still one of Aunty’s favorites – their beef stew is delicious as well as their tofu sandwich.)

Mahalo much, Yunji! So glad to have a nice new niece!

Aunty just recently subscribed to Bug Free Mind’s free trial offer – 5 chapters of the program and access to their website (after registering and logging in). Aunty also joined as an affiliate to the program – just in case this really is what it promises to be. A review of the program will be forthcoming, but it really does seem to be mind set changing – the first change necessary for any improvement in our lives. Rich Dad Robert Kiyosaki preaches this all the time, and his Cash Flow game changes one’s mindset from stuck in the rat race to unlimited passive beautiful income.

An article in the Bug Free Mind website was entitled “3 Magic Words that Eliminate Stress Immediately!”

Hmmm. What could those be? “You won $1,000,000” would work for Aunty. “Honey, I’m home!” used to work long ago in the honeymoon phase of marriage. “Just go shopping” was an action that used to work wonders.

Well, according to the article, those 3 magic words are, “Accept what is.” Hmmm. Accept what is.

It almost sounds too simple, but on further reflection, they are words of wisdom and really can relieve stress. Try it out on a situation in your life that creates stress. Acknowledge that the problem, condition, circumstance exists, because it does. It is what has happened, what is, and all the worrying and stressing about it does not change it. Glare at it, swear at it, cry over it, and then accept that that is what you own.

The magic happens after that – when you can look at those stress producing piles of crap and decide on a plan of action to eliminate or deal with them.

Can’t figure out a plan of action? Another article in the Bug Free Mind says to sleep on it. Just before falling asleep, ask the questions for which you have no answers. “What can I do to improve my relationships?” “How can I pay my bills?” Ask, out loud or silently, just before you drift into slumber.

In the morning, in those first 10 – 20 minutes of arising, the answer(s) may be there. If not, repeat until you get the answers.

Does it work? It doesn’t hurt to try. Aunty will try and let you know later. Let Aunty know how it goes for you, mahalo.

[note from Aunty: once you register for the free trial, a rather aggressive email campaign to get you to opt into the full program will begin. Aunty’s suggestion is that you just ignore these for now, just get the free stuff, cruise through their website before signing up for anything more. The good thing about their aggressive email campaign (done with excellence, btw) is how your affiliate relationship with them is supported automatically.]

Happy New Year! Aunty wants to start the year blogging with some self improvement, and the ability to persuade is a good tool in anyone’s belt. Here’s a book report from Aunty:

The other day, Aunty was sitting next to Uncle and telling him about one of her very interesting revelations (Aunty gets revelations quite often). In Aunty’s telling of it, Uncle looked at this watch. Aunty got ticked off and stopped in mid sentence. You see, to Aunty, that action meant that he wasn’t really listening, and that he was bored.

Uncle, being a nice guy, begged me to continue, but the moment of me wanting to share a revelation with him was lost in the cloud of being insulted (in Aunty’s own mind.)

Who was at fault? To hear Uncle apologize it would seems as if he were. However, after a time of reflection, I do believe the fault was my own – my spoken word bored him, and probably would not engage anyone else who had the misfortune of listening to my dissertations.

Aunty can write easier than speak, especially with spell check and thesaurus tools on the computer. Writing is non invasive. It is the other person’s choice to read, versus the spoken word is invasive. Anyone in earshot will hear the words, whether they want to or not.

So, it is now one of Aunty’s goals to become a better speaker – one that can hold and capture an audience rather than bore or irritate them. That means a whole lot of training, learning, and practicing.

Here is a TED video by Julian Treasure on how to speak so others listen:

One way to practice is to join a local Toastmasters Club – one item on Aunty’s to do list. Aunty’s favorite way to learn is on the internet, searching for ideas and resources. During a search for a great speaking guide, Aunty found a book, “Resonate, present visual stories that transform audiences” by Nancy Duarte. Wow! Just the title had me hooked – Aunty can transform audiences!?

[First off, the author has made it easy for a skim reader like Aunty. She highlights gold nuggets of information for skimmers with bold text, references with green, items of deserved emphasis with orange. The book is filled with outstanding speeches of famous people that she used as examples of excellence. She has a website: www.duarte.com, a goldmine of information.

Turns out, this book is more about presentations in front of an audience – more of a communication goal that is oriented to persuasion. This could work – more of a jump into a bonfire than a flame, but Aunty is game!]

Here is a TED talk that Nancy did in 2010:

Here is Aunty’s book report:

To resonate, you must tune your message to your audience’s minds, needs, wants, rather than expect them to tune into you just because you are speaking. It will take work on your part, with an ebb and flow of content, emotion, and delivery. Make it about your audience. If your ideas stand out, they will be noticed. Stories are the most powerful delivery tool for information. [Einstein once said, if you want your child to be creative, read them fairy tales. If you want them to be more creative, read them more fairy tales.]

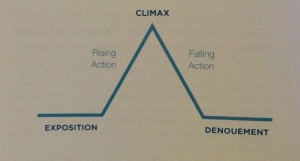

Blending information with stories creates a perfect world for a presentation. Stories have 3 parts: a situation, a complication or conflict, and then a resolution. A great presentation should have a clear beginning, middle, and end. The first plot point in an incident that captures people’s attention with intrigue and interest is called a turning point. In a presentation, this turning point may be an idea, or a solution to a problem, or some kind of conflict or imbalance perceived by your audience that your presentation resolves. You can also create imbalance by juxtaposing what is with what could be.

The contour or form of a great presentation:

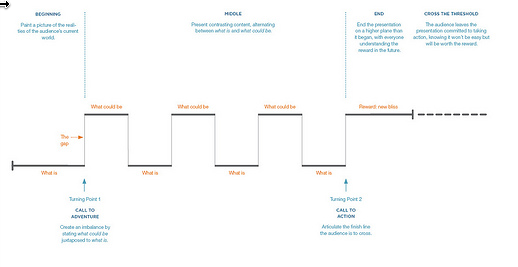

The Beginning paints a picture of the audience’s reality – this is the what is. The beginning comes before the first turning point. It is historical and the present, often including a problem that the audience has in common. Create a common bond with the audience. That can be short and should not take up more than 10% of the presentation. Then, create a call to adventure, putting forth a memorable big idea that conveys what could be.

The Middle is the contrast, that first turning point of the call to adventure, and will be made up of various types of contrasts of dilemma and resolution, dilemma and resolution. The middle is continuous back and forth between what is and what could be. This alternating between the two, the present and the possibility pushes and pulls the audience to feel as if events are constantly unfolding, and they will be engaged and interested, wanting to learn how to resolve the imbalance in their lives or achieve what they want. It is very important to know your audience so that you can understand your similar or opposing views. Content that is oppositional to their belief is stimulating. Familiar content is comforting. The call to action gives your audience tasks that they can perform, depending on what type* of person they are – a doer, supplier, influencer, or innovator. All are important, all can be reached if you provide each type with at least one action that they would be comfortable in performing.

The End of the presentation is concluded with the resolution, a vivid description of the new feeling of bliss that is created when what could be is achieved or reached, and a willingness to be transformed. Let the audience know what the finish line will look like, ending it on a higher plane of enthusiasm with everyone understanding their future rewards.

It is important that the audience leaves the presentation committed to taking action, that they make a decision to cross the threshold. T.S. Eliot said “What we call the beginning is often the end. And to make an end is to make a beginning. The end is where we start from.”

*Four distinct types and profiles of people:

Doers – instigate activities, the worker bees. They recruit and motivate other doers to complete important activities.

Suppliers – get resources. These are the ones with financial, human, or material resources. They have the means to get you what you need to move forward.

Influencers – the ones who can change perceptions of others. These people can sway individuals and groups, mobilizing them to adopt your ideas.

Innovators – idea generators. These are the ones that think outside the box for new ways to modify and spread your idea. They create strategies, new ways of thinking, products that are new.

The Sparkline

The author has a line tool that she calls a sparkline. It consists of the Beginning, and then a series of stories or details about what is followed by what could be with sparkles and star moments sprinkled in. Towards the end of the presentation are contrasting emotion and delivery, and then the call to action that defines what your audience CAN do, followed by the End that paints a vivid picture of the potential reward.

An example of a presentation with all the components of a perfect presentation that leads to the transformation of audiences is Benjamin Zander in his 2008 TED talk. Go to TED.com, search for Benjamin Zander, and enjoy. Chopin anyone?

Get to know your audience

Instead of the old school way of imagining your audience in their pajamas to get over your fear of speaking in front of them, imagine them as a line of individuals waiting to have a face-to-face conversation with you. The audience must be your focus – it is about them, not about you.

Do research on your audience, the more you know who they are, the better you can structure what you say to connect and move them. Figure out what your audience cares about and link it to your idea. Give them something that they didn’t know before, create common ground. Success is having your idea be understood and accepted as a great idea by them.

The Big Idea

Determine what your key message is. This is your goal – it needs to be a complete sentence so it is easily articulated and can be repeated. The message is your Big Idea. It must convey what is at stake (what is compared to what could be), and it must be specific, not a generalization such as “be happy.”

Once you have the Big Idea, identify where your audience is at right now, to where you want to move the audience to. Changing beliefs means changing actions. If they can shift their beliefs to be able to accept your ideas as a viable path, then guide them toward the actions that can get them unstuck from their former beliefs in order to have a reward that is worthwhile for themselves, their sphere of influence, and perhaps even the world.

Every audience will persist in a state of rest unless compelled to change. It is your job to compel them. To do this, you must first assess, and then deliver what they want.

Assess and deliver by meeting the heroes

Look upon the audience as a room full of heroes. Figure out what they care about and link it to your idea. Be mindful of how you fit in their lives in order to guide them and bolster their confidence in you.

Figure out what your audience cares about and create a link between that and your Big Idea. They need to leave your presentation knowing something that they didn’t know before – the aha moments are powerful, and YOU gave it to them! If you have any common ground with them, use it to make a better connection.

The journey of the Big Idea

First off you must define the destination that you want your audience propelled to. Map it out and be prepared for resistance. When resistance is harnessed properly, it can create forward progress towards acceptance of the one key message you want to communicate – the Big Idea.

The 3 components of a Big Idea:

A Big Idea must be your point of view, not a generalization.

A Big Idea must convey a sense of urgency and importance.

A Big Idea must be a complete sentence that you can articulate.

Use the 2 emotions of pleasure and pain to make your point by raising the likelihood of pain and lowering the likelihood of pleasure if they reject the Big Idea or vice versa, raising the likelihood of pleasure and lowering the likelihood of pain if they accept the Big Idea.

Map out the journey that you want for your audience, moving them from inaction to action, from stuck to unstuck. You are asking them to change. Acknowledge them for it by acknowledging the risk, sacrifice, or their fears. Contemplate all the ways that your audience may resist and address them, at the same time assuring them that the Big Idea is a good one.

The benefits of the Big Idea should appeal to their basic needs such as security, savings, winnings, recognition, improving relationships, achieving goals, or their full potential. Some may refuse or resist the call to action. They need to feel that they are in good capable hands – your hands. They also need to feel that taking action is worth the risk, because of what the reward or payoff will be. [Jeff Olson, says, “the price of neglect is far higher than the price of discipline.]

Create Meaningful Content

Use sticky notes to jot down ideas, facts, stories, projects, possibilities, etc. – anything that supports your presentation. Collect ideas from a multitude of sources, create ideas, and write them down everything that you can.

Have a balance between logical, emotional and ethical appeal.

Think about the issues of opposing points of view for this may give you more ideas for your presentation.

Most great presentations use personal stories. Draw on your past experiences with people in your life, places you have been, or things that can enhance your points. The best stories follow a standard flow – description, problem or conflict, solution. When you can turn your own data base of stored memories and images into stories, you are transforming information that is charged emotionally and makes it more digestible and believable, as well as enjoyable to the audience.

Edit, and edit some more.

Keep in mind the Big Idea. Filter in order to make it clear, not overwhelming your audience with too much information no matter how relevant you might think it is. Slash and delete so you end up with the best stuff in a smaller format. It is easier to digest for your audience.

Structure your content

Presentations need to feel organized. Structures help to hold everything together. The most widely used structures are outlines, or a logic tree – giving viewers a snapshot of looking at the whole and not only the parts.

Order your information from the Big Idea or problem to what it is now to what it can become. When you create interaction with emotional responses (i.e. laughter, sympathy) and alternate it with analytical content, your audience will feel and be affected. Avoid reading from the screen – you want human connections, not route readings.

When using slides, present one message or idea per slide. Keep it simple. Use cartoons or pictures that represent words. A solid structured presentation will cause ideas to flow logically and helps the audience see and feel the Big Idea along with you.

Give them something to remember

You want to give them something that is significant, that they will be talking about or thinking about for a long time. Five types of significant moments come from:

memorable dramatizations – Steve Jobs, when introducing the MacBook Air, pulled it out from a manila envelope

repeatable sound bites – imitate a famous phrase, a rally call, a crisp message that people will want to repeat to others

evocative visuals – something that moves the audience

emotive storytelling – share from your own personal experience or feelings

shocking statistics – show a graph, chart, comparison that give the viewer a sense of urgency.

Improve

Give a positive first impression.

Speak in the language and manner that will reach your target audience.

Keep it short – a prime example of this was Lincoln’s Gettysburg Address, which lasted only 2 minutes and consisted of just 278 words.

Move away from presenting from slides or use slides just to help your audience recall your message.

Create the right balance of emotion, facts, credibility. Too much or too little of any of these components may leave the audience feeling manipulated.

Practice in front of critics and listen to their feedback.

No matter what the subject matter, practice and practice again to make it perfect.

Changing the World is hard

Creating begins with an idea that can change the world. Change will bring about challenges and resistance. Sometimes you must put your reputation and popularity on the line in order to advance what you believe in. Don’t give up.

Your idea becomes alive when it is adopted by another person, then another, then another until it becomes a groundswell of believers in support. Presentations can be the vehicle to communicate your vision and get support. If your message is done well and moves your audience to action, using the social medium phenomenon of YouTube, Facebook, and others will get your message repeated and possibly viewed by millions.

Be the real you, be transparent. To do this, be honest, be unique, and don’t compromise.

Believe in yourself and your ideas, and others will follow.

Closing

We all have ideas that are potent. If it is a great idea that can change the world for the better, go for it. Communicate your idea in the best way that you can. Gather, prepare, learn from prime examples, write, rewrite, get feedback, and then send your message out to the audience. Change the world!

Aunty’s note: This book took Aunty over 6 months to finish, perhaps because it was just not in Aunty’s sphere of comfort. Aunty’s mind would wonder during chapters. However, if you are in a job or occupation that requires public speaking, this book is an excellent source to help get your point across and into your audience. Next step for Aunty – pick a goal, work on the presentation, and go present it to Uncle. If done well enough, Uncle will say “YES!”

Being part of HiREI has many benefits, and one of them is being part of the women’s group, Hawaii Women Real Estate Investors (HiWIRE for short).

The October HiWIRE meeting was sparsely attended with Gary DeBose as the featured speaker. Gary has done hundreds, if not thousands of deals, most of them using other people’s money and other people’s talents to find/purchase/fix great real estate buys, and sell at large profit margins.

Gary’s style of presentation borders on insulting, and he admits that from the very start. You may decide to bolt out the door, but Aunty sat her butt down and stayed put. It was a good decision even though Aunty’s strategy and long term goal is buy and hold, cash flow rental income from real estate.

Aunty’s notes were very sparse because he talked a mile a minute and his figures, calculations, and projections were presented in rapid fire. The gist of it all was that you could make excellent money buying low, fixing and/or repurposing, and then selling high.

Cash flowing rental real estate is not his goal

His goal is to buy, fix, sell – quickly, cheaply, for as much profit as possible.

One current deal that Gary is working on is a hotel complex – Holiday Inn in a semi rural area on the mainland near a freeway. This Holiday Inn was losing money because of poor occupancy. Using $3,000,000 of investors’ money, Gary secured the title wrapping around the seller’s mortgage (strategy that Aunty has never done), is in the process of renovating the entire complex into a resident care facility (senior citizen home), renting out units until fully occupied and cash flowing at $64,000 per month, and then selling it for $23,000,000. This will net his investors more than double of their money, and a very tidy profit for himself.

This was Wowza. Very Wowza.

Gary has the vision, know how, and fortitude to max out profit, and he does it with a set of formulas and street smarts to get it done.

However, this was NOT a case of, “if he can do it, anybody can do it.”

No, because Gary lives, breathes, and consumes real estate. He puts in a lot of time, talk, and non stop thinking, planning, negotiating, implementing, teaching, growing, presenting, traveling, and juggling. He has a team of hundreds working with him. He is a bulldozer. A very admirable, somewhat abrasive, brilliant bulldozer.

Two ways to join

One of the ways to join Gary’s team is to be a finder of deals. This means you are doing a lot of research, knocking on doors, finding distressed situations, running numbers. If it turns out to be an acceptable property that turns a profit, you get paid a nice fat fee after the property is sold.

Another way is to put money in Gary’s hands (via escrow) and ride behind the bulldozer with him. Results are not guaranteed, but you do get to pick your deal. In some cases, you get paid your portion back plus a tidy return in weeks. In some cases, it may take a couple of years (the Holiday Inn example).

Aunty in the wrong strategy?

After hearing Gary’s presentation, Aunty’s world felt a little knocked over. It seemed to make so much more sense to flip real estate rather than rent and hold. The ROI (return on investment) can be SO much higher doing flips rather than rentals. Why buy and hold for returns of 8%, when you could buy and flip and get returns of 20%, 50%, 200% or more?!

Aunty found herself in a quandary – a state of uncertainty. Not a good feeling for Aunty. Should we be flipping instead of going for cash flow? Aiyaayaa (pronounced eye – yah – yah) – aiyaayaa!

The very next day, as if the sound of angels’ harps strummed through the air, a calmness came over Aunty, and her world was righted back to square. It came after reading a quote in one of the many (many) newsletters that come into my email inbox last night:

“Everything we hear is an opinion, not a fact. Everything we see is a perspective, not the truth.” – Marcus Aurelius

Aunty can buy/hold/rent and be okay. Gary can buy/fix/flip and be awesome. That was a very nice A-ha moment.

Stick to your guns, even if they are slow

There are several pros and cons for flipping or renting for real estate. [note to Aunty (and please remind Aunty if she forgets..) – write a more detailed post on those pros and cons.]

Most of the speakers that have programs or a call to action for you to join are flippers. Flipping is a rush. It is exciting to buy low and sell high. It is fast money – you get a return of you money PLUS a nice sized profit in a short period of time. It works beautifully, until it doesn’t. Robert Kiyosaki (Rich Dad, Poor Dad fame) calls it linear income – you do a deal, make money, and in order to make money again, you have to do another deal.

Buy and hold income, on the other hand, is not fast. It is slow, but steady. Successful rental real estate will continue to pay you with rental income month after month, year after year, whether the value of the property goes up or down. It’s not exciting, but having cash flowing rental real estate in the right places helps you sleep at night.

Aunty learned not to share what she does with flippers

The reason is that experts who do short term flips can poke enormous holes in Aunty’s and Uncle’s portfolio and strategy. They would be absolutely right in their analysis for their own intentions. They would be not right for ours.

Besides Robert Kiyosaki’s sage advice, Aunty also pays attention to Jeff Brown of BawldGuy.com. He builds a blueprint for clients ($3,000) – even for clients that don’t always follow his advice (ahem, perhaps Aunty needs to learn to listen to him better). Please read an article he wrote for Bigger Pockets back in May 2012, “What’s your End Game?” This was an excellent article about investing to grow funds rather quickly in order to be able to slow down later.

Flip to make money

Does Aunty ever do flips herself or with others in joint ventures? Yup, you betcha. The best way Aunty has found to do short term flips is in a checkbook Roth IRA because of $0 taxes, and zero tax filing requirements. Zero!!!

We sometimes flip in joint ventures by forming an LLC in Hawaii (cheap – lucky we live Hawaii). Our Hawaii LLC goes into a contract as a partner, or sometimes just as a lender, the controlling partner does all the wheeling, dealing, arranging, paperwork, etc. and at the escrow closing or other agreed upon time, we get our investment back plus profit or dividend (for which we file on our tax return and pay taxes). Gary DuBose could be someone that we would invest money with – if and when we have enough to do so with. His minimum investment criteria is $100,000 with potentially awesome returns.

What Aunty learned

Gary DuBose is a certifiable and proven expert that knows how to make a ton of money flipping real estate. He flips for his income, we do not. Regardless, Aunty is grateful for the information that he shared with us at the HiWIRE meeting.

Of great value to Aunty are a couple of tools for evaluation that he gave to us:

bestplaces.net is a website that is free and very useful. Enter the zip code of the area that you want info on in order to see tables listing by population overview, statistics, and info galore. For real estate purposes, select the “Housing” link. Make note of the information given for the average household size (HS) and average household income (HI). These numbers are specific to the zip code that you input.

Apply these numbers to Gary’s formula of HI/HS x 1.85 x .31. In human talk, that is Household size, divided by Household income, multiplied by 1.85, and then multiplied by .31. Divide this number by 12 to get a monthly figure. This monthly figure is what you could expect to get as monthly rental for an average 3 bedroom house.

Next, go to rentometer.com. Enter the zip code or address of the property you are researching and input that number (expected monthly rental) into the rent/mo box and the number of bedrooms of the unit. This website will compare your property to others in the same neighborhood and show if it is too low, too high, or just right.

Another great and very simple tool to find out what your mortgage payment will look like for any loan amount at a specific interest rate is Karl’s Mortgage Calculator. This is an easy way to find out what your mortgage principle and interest payment will be – taxes and insurance are not included.

Mahalo to Gary and HiWIRE

Aunty did not go this month’s HiWIRE meeting with any expectations other than meeting up with Martha to give her a book (The Slight Edge by Jeff Olson), and to socialize with the other wonderful ladies. It turned out to be a powerhouse meeting that had me wired (oboy) for hours after because of SO much information from Gary.

Gary does have a website: thedealfunders.com with his contact info and upcoming events.

Aunty is very glad that she set herself down, put on her listening ears, and came away with much more than when she arrived. Gary even sang his latest marketing jingle – what a great voice!

In retrospect, Gary sorta kinda looks like Honolulu Bulls head coach, Phil Neddo. Both are bulldozers, both are fearless, both are sons of preachers. Hmmmm. I wonder if Phil can sing?

Aunty did a post about selling on eBay a couple of years ago. Aunty also took (paid some bucks) an eBay course from an eBay guru who was a power seller. Truth to tell, Aunty did not use much of the information since a lot of it was for true rookies and some were for power sellers that are willing to devote all of their time loading, selling, packing, and shipping.

Aunty did a post about selling on eBay a couple of years ago. Aunty also took (paid some bucks) an eBay course from an eBay guru who was a power seller. Truth to tell, Aunty did not use much of the information since a lot of it was for true rookies and some were for power sellers that are willing to devote all of their time loading, selling, packing, and shipping.

Aunty went to a

Aunty went to a  !!!!Update added at end of this article.

!!!!Update added at end of this article. Recently, Aunty has been reading about the Chinese yuan (or renminbi) becoming a world reserve currency when the IMF (International Monetary Fund made up of international bankers) meets in October. If this happens, then international trades, purchases, exchanges, etc. can be done with Chinese money. Currently, the US dollar is the dominant trade currency, followed by Euros, English pounds, and Japanese yen. Adding the Chinese yuan to the mix may have extreme financial consequences.

Recently, Aunty has been reading about the Chinese yuan (or renminbi) becoming a world reserve currency when the IMF (International Monetary Fund made up of international bankers) meets in October. If this happens, then international trades, purchases, exchanges, etc. can be done with Chinese money. Currently, the US dollar is the dominant trade currency, followed by Euros, English pounds, and Japanese yen. Adding the Chinese yuan to the mix may have extreme financial consequences.

Aunty likes to talk to strangers, especially when waiting in lines or when nothing is going on.

Aunty likes to talk to strangers, especially when waiting in lines or when nothing is going on. All Mālama Card merchants are located on Kamehameha Schools’ commercial properties. These properties include Royal Hawaiian Center, Windward Mall, Pearlridge Center, Kahala Mall, Kapālama Shopping Center, as well as Waipahu, Waiakamilo, Kaka’ako, Keauhou, and Hawai’i Kai. Income from the school’s commercial leases fund KS’ campus and community outreach programs throughout the state.

All Mālama Card merchants are located on Kamehameha Schools’ commercial properties. These properties include Royal Hawaiian Center, Windward Mall, Pearlridge Center, Kahala Mall, Kapālama Shopping Center, as well as Waipahu, Waiakamilo, Kaka’ako, Keauhou, and Hawai’i Kai. Income from the school’s commercial leases fund KS’ campus and community outreach programs throughout the state.  Aunty just recently subscribed to Bug Free Mind’s

Aunty just recently subscribed to Bug Free Mind’s  The other day, Aunty was sitting next to Uncle and telling him about one of her very interesting revelations (Aunty gets revelations quite often). In Aunty’s telling of it, Uncle looked at this watch. Aunty got ticked off and stopped in mid sentence. You see, to Aunty, that action meant that he wasn’t really listening, and that he was bored.

The other day, Aunty was sitting next to Uncle and telling him about one of her very interesting revelations (Aunty gets revelations quite often). In Aunty’s telling of it, Uncle looked at this watch. Aunty got ticked off and stopped in mid sentence. You see, to Aunty, that action meant that he wasn’t really listening, and that he was bored. Blending information with stories creates a perfect world for a presentation. Stories have 3 parts: a situation, a complication or conflict, and then a resolution. A great presentation should have a clear beginning, middle, and end. The first plot point in an incident that captures people’s attention with intrigue and interest is called a turning point. In a presentation, this turning point may be an idea, or a solution to a problem, or some kind of conflict or imbalance perceived by your audience that your presentation resolves. You can also create imbalance by juxtaposing what is with what could be.

Blending information with stories creates a perfect world for a presentation. Stories have 3 parts: a situation, a complication or conflict, and then a resolution. A great presentation should have a clear beginning, middle, and end. The first plot point in an incident that captures people’s attention with intrigue and interest is called a turning point. In a presentation, this turning point may be an idea, or a solution to a problem, or some kind of conflict or imbalance perceived by your audience that your presentation resolves. You can also create imbalance by juxtaposing what is with what could be. It is important that the audience leaves the presentation committed to taking action, that they make a decision to cross the threshold. T.S. Eliot said “What we call the beginning is often the end. And to make an end is to make a beginning. The end is where we start from.”

It is important that the audience leaves the presentation committed to taking action, that they make a decision to cross the threshold. T.S. Eliot said “What we call the beginning is often the end. And to make an end is to make a beginning. The end is where we start from.” The Sparkline

The Sparkline Assess and deliver by meeting the heroes

Assess and deliver by meeting the heroes Structure your content

Structure your content Being part of

Being part of